In an ever-expanding financial world, it’s vitally important that institutions and their customers are protected from criminal activity, and that those who help facilitate it – directly or indirectly – are prevented from doing so via strong regulatory controls. The know your customer process, usually known as “KYC”, is a set of identification and verification checks banks and other institutions must carry out to ensure that the customer is who they say they are.

In the case of individual customers, this process generally consists of photo-ID checks, address verification and in some cases a live face verification, though it can vary depending on the regulatory body in a specific jurisdiction. It’s also important to check specific anti-money laundering watchlists for potential matches with sanctioned individuals, convicted criminals or PEP (politically exposed persons) who might be exposed to corruption, bribery or other financial crime.

If the client is a business, the checks are more complicated. In this case it is key to map the shareholding structure of the company and to verify the main Ultimate Beneficial Owners, or UBOs, of the company under KYC investigation. UBO identification is vital to the ongoing effort to combat money laundering and terrorist financing.

What is KYC?

The term KYC, or Know Your Customer, describes the process banks and other financial institutions carry out to verify the identity of a customer. This process is outlined by both international and national regulatory bodies and is a key part of the ongoing effort to combat money laundering, terrorist financing and other serious financial crimes.

While the exact steps can vary depending on the industry or the market being operated in, the general principle when it comes to KYC verification of individuals is the same – the customers must be verified via document checks, photo-ID and proof of address (e.g. utility bills, voters’ registers) as well as potentially live face verification and the collection of biometric data.

The objective of these checks is to deter criminals from attempting to access financial services that could be abused for money laundering and terrorism financing. The KYC process then has a twofold effect for regulated businesses – not only do these checks help ensure that financial crimes are easier to spot and harder to commit, they are also demonstrating to legitimate customers that the business in question values their information security and is actively taking steps to prevent the misuse of their identity, because by verifying a customer’s identity you mitigate the risk that it’s being used fraudulently.

Delving into UBO – The Ultimate Beneficial Owner

In the case of corporate customers, one of the most essential aspects of anti-money laundering due diligence is investigating the ownership structure of such businesses. The UBO, or Ultimate Beneficial Owner, refers to the ultimate beneficiary of any dealings or transactions a corporation makes. Typically that’s the owner or the person who controls the company, but it’s important to also understand that this does not necessarily need to be the named owner, just the person or persons that benefit the most. In simple terms, the legal owner is the person who is named as the owner on paper, but the beneficial owner is the person who has control of the decision making and reaps the financial reward of any transactions.

Because corporate entities may be used to mask financial crimes and as a way to launder illicit profits, it’s vitally important that the UBO of an entity is established clearly in the KYC process. Again, this serves two purposes – it firstly establishes transparency to prevent financial criminals from concealing their ownership, but it also protects institutions from fines and reputational damage. Criminals will never stop working to obscure both their illegal activities and their identities and banks have a pivotal role to play in preventing these crimes from happening.

The Role of UBO in KYC Compliance

Being strict on the disclosure of UBOs is the key to combating major financial crime. If a company is being used as a shell to obscure money laundering activity, having identification data for its UBO will make the process of tracing the source of illicit funds a lot more straightforward. Even in the case of more complicated ownership structures, it gives regulators a breadcrumb trail to follow, and provides a strong deterrent to would-be criminals.

Dealing with these complicated corporate structures is arguably the biggest challenge facing financial institutions today, and identifying the relevant UBOs is a key aspect of this process. Being able to pick through multiple layers of legal ownership, identifying shell companies, examining share structures to pinpoint the common thread of ownership is a vital skill for financial institutions to pick up, and the risk of ignoring these practices is becoming more apparent every day.

Indeed, one does not have to look too far from major news sources to find examples as to why this process is so important. In the UK, Xpress Money Services were issued a £1.4 million fine for breaching AML regulations – this included a lack of due diligence when it came to investigating beneficial ownership. They have since entered administration. Recently in Hong Kong, a fine of $764,000 was levied at Commerzbank for, among other offences, failing to implement name screening mechanism of customers’ beneficial owners during this period.

Singapore, too, is taking action – recently the Monetary Authority of Singapore issued a series of penalties related to failures in UBO identification totalling $3.8 million. The largest individual penalty was issued to DBS for failures in their due diligence on the beneficial ownership of certain customers, as well as failing to update their risk ratings. To read more in depth about this story in particular, click here for a more comprehensive article.

Steps in Identifying UBO

Considering the risks, it’s important to understand exactly how UBO status is determined. The UBO of an entity is explicitly defined by the FATF (the Financial Action Task Force) as someone who has a stake of at least 25% in the capital of the company, has at least 25% of the voting rights and is the beneficiary of at least 25% of the capital. Company registries represent the most reliable source of information when it comes to understanding the ownership structure of a registered business and the effective control power of an individual beneficiary. For example, the same individual might be the owner of four companies registered in different countries, each one of them owning 10% or less of the business under KYC investigation. Only by accessing the registry in each one of those countries, using official documents to identify who owns each of those four companies, and mapping the subsequent corporate structure, a compliance officer will realise that there is a key UBO of the company under investigation who actually owns 40% of the business.

As a threshold, the 25% ownership limit is a useful starting point as all of this information can be usually verified with company documents, but in order to meet other KYC obligations the UBO’s identity and wealth status must be vetted further.

Once identified, vetting a UBO is initially similar to other KYC practices – their identity will need to be verified via documentation, photo ID and proof of address, but they will also need to be checked for other signs of financial crime. Checking their name against sanction databases and PEP (Politically Exposed Persons) lists is also key to ensure that the UBO is not involved in any scandals or has the potential to be exposed to corrupt activity.

Challenges and Solutions in UBO Identification

Due to the complex nature of this process, identifying UBOs can be a challenging task, particularly when operating on a global level.

Many economies around the world simply don’t have a framework for collecting UBO information from registered companies, which can present financial institutions with large investigative hurdles. Even countries that have attempted to introduce UBO registers – such as various ones in the EU – have encountered some problems, as UBO registers have conflicted with data protection laws in some areas, leading to a muddled field full of incomplete data. For institutions trying to do the right thing, these kinds of issues can create huge inefficiencies in the gathering of data, leading to delays in the delivery of services.

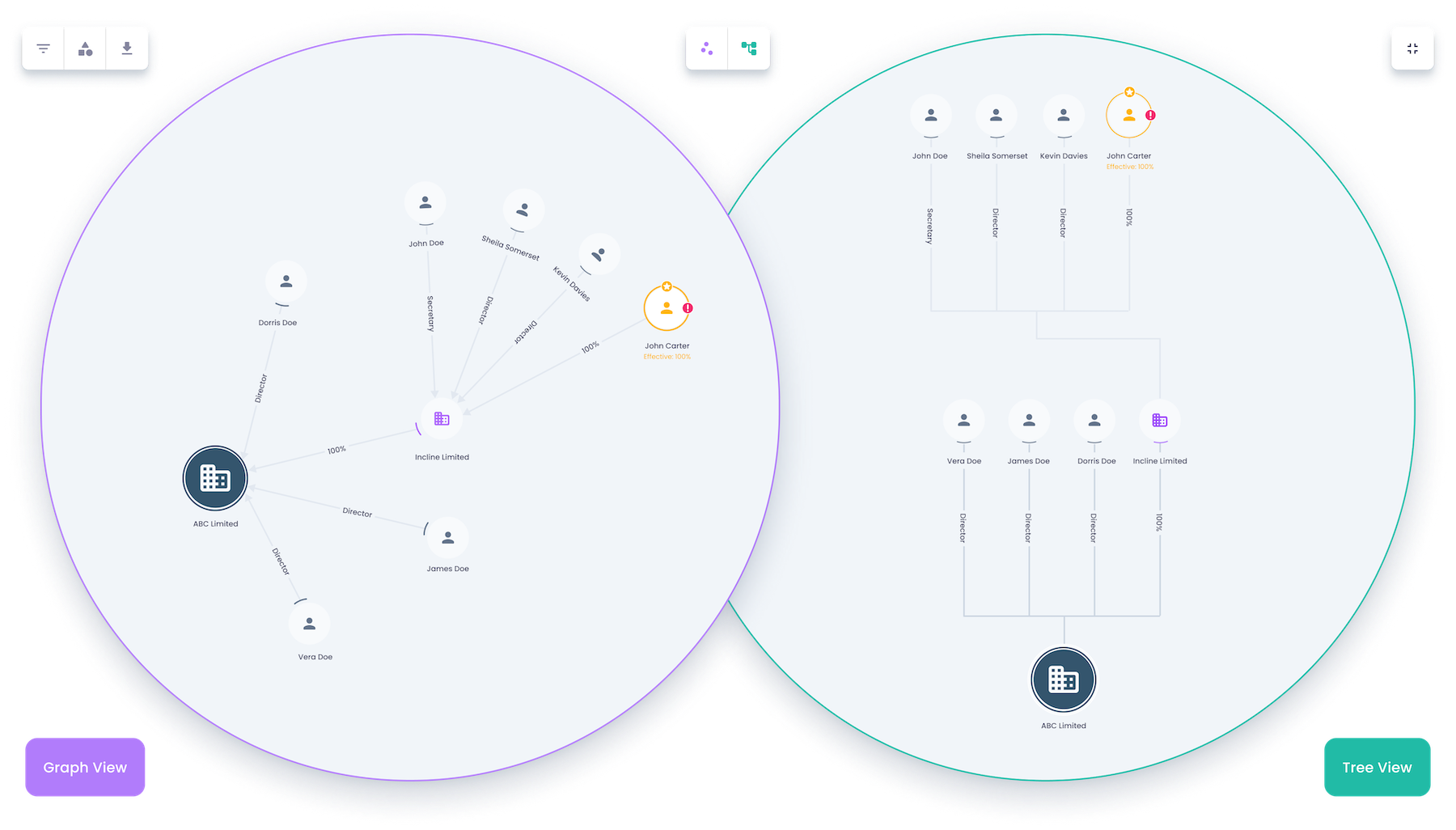

As a result, it’s increasingly important for financial institutions to be aware of the latest technological solutions to help smooth their UBO Identification processes. Utilising a dedicated cloud-based platform to centralise and streamline all your AML and KYC checks, you’ll be able to leverage automation to increase the speed and accuracy of corporate structure mapping and UBO identification. RegTech vendors like Know Your Customer offer time-saving functionalities helping compliance teams clearly visualise the chain of ownership in complicated corporate structures no matter the regulatory market the business is operating in. For compliance teams, it is very important to ensure that the data showcased in these highly intuitive graphs is sourced by reliable and up-to-date sources such as official company registries, and not from static databases only updated at intervals.

Know Your Customer’s Ownership Structure Charts present vital UBO and AML information in highly intuitive visualisations. All data showcased in the graphs and tree views is sourced in real-time exclusively from official company registries to ensure maximum reliability and transparency.

Recognising the importance of proper UBO identification is an essential step towards maintaining a strong KYC foundation. The unfortunate truth is it’s a challenging task. As criminals develop more complicated corporate structures to obfuscate illegal assets, financial institutions will have to continually evolve their KYC processes to stay one step ahead, making use of every tool available to develop a comprehensive solution.

Now more than ever, it’s critical for compliance teams to stay informed and up to date with the latest anti money laundering protocols, and ensure that their institution is compliant with all current regulations. For weekly updates on all things KYC, AML and RegTech innovation, you can follow Know Your Customer on LinkedIn and Twitter, or subscribe to our general newsletter here.

If you’d like to learn more about leveraging best-in-class software solutions in your own KYC checks, click below to get started.

Last updated on April 16th, 2025 at 02:09 am